Listen, homebuyers fondly remember that brief, beautiful fever dream where mortgage rates lived in the 3% to 4% basement. But since 2023, we’ve been stuck in the 6% penthouse, and frankly, the view isn’t worth the price of admission.

You’ve seen the news. Inflation is “cooling.” Interest rates have “dropped.” So why are your local bank still looking at you like you’re crazy when you ask for a deal? Let’s break down the chaos.

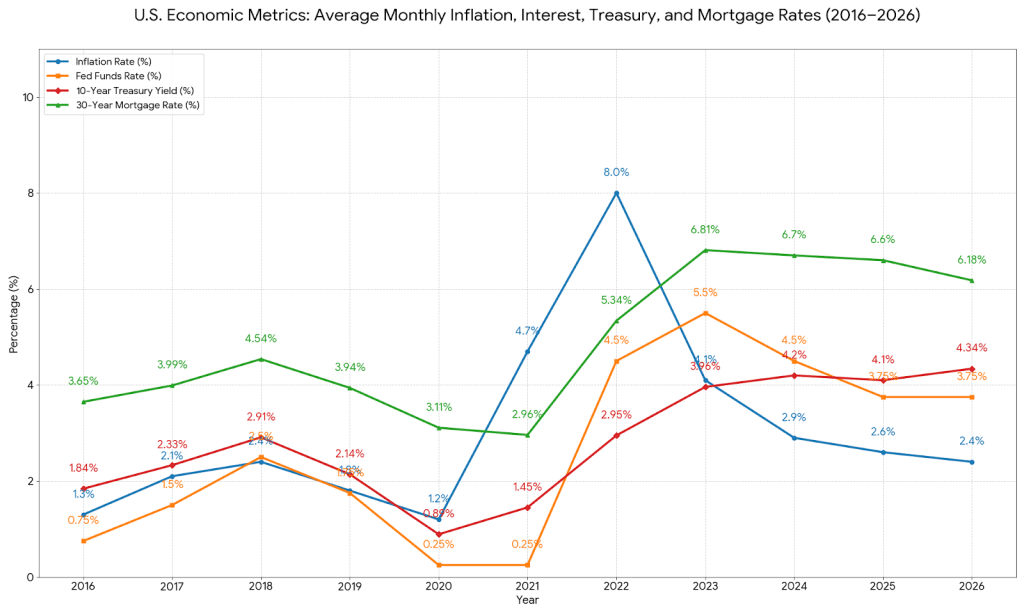

For those of you like charts and numbers (We do!), here’s one showing the how average monthly 30-mortgage rates have increased (the green line) and the big drivers inflation (blue line), interest rates (orange line), and 10-year treasury yields (red line) over the last ten years. Notice the big bumps in 2021 and 2022. Let’s see what’s going on in this mess…

Phase 1: The COVID Hangover (2021–2022)

Remember when everyone was stuck at home and decided they suddenly needed an air fryer and a home gym? Well many people who were needed to make the stuff that you wanted were also stuck at home or absent or sick. Even though they kept making stuff, they couldn’t make enough stuff to keep up with the demand given all the COVID-19 restrictions. Pair that with the US government handing out rebates and expanding social programs like a billionaire at a gala, and we’ve got even more money for people to spend and drive up demand. Well basic economics says that when demand for products outpaces the supply, prices increase. And that’s inflation. In this case, massive inflation because of the size of gap sending the Blue Line (Inflation Rate) screaming towards an average monthly rate of 8% in 2022 (peaking at almost 9% for a few months)

To stop the bleeding, the Federal Reserve did the one thing it knows how to do: it cranked the Orange Line (Interest Rate) up to the 4.5%–5.5% target range to purposefully slow the economy down. The interest rate in this case is actually the Federal Funds Rate, which sets the borrowing rate between banks. We won’t go into all the reasons the Fed does this but it’s a historical lever they’ve pulled in the past to fight inflation.

Phase 2: The Treasury Bond Yield Cycle

Once interest rates go up, 10-Year Treasury Bond Yields will follow. So what are these treasury bond yields? Well, that’s how the federal government funds its debts. An investor pays $1,000 in 2021 for a treasury bond and then 10 years later the investor gets their $1000 back plus a little extra each year they held the bond. The higher the “yield” the more money the investor makes. However, if investors can get a quicker return through other investments with a higher interest rate (say 4.5-5.5%), they’re not going lock themselves into a 10 year investment for a lower return. So, when interest rates and inflation went up in 2020-2021, the Red Line (10-Year Treasure Yield) went up to almost 4% to satisfy those investors.

Alright, at long last… that leads us to mortgage rates. Banks loan money to people to buy property and give them 10, 20, 30 years to pay it back plus a little extra each year. Sound familiar, right? Because banks see mortgages as long-term investments, they look at those treasury bond yields and say, “We want that rate, plus 2-3% more for our trouble”. And lo and behold, looked our Red Line (Treasury Bond Yield) at just under 4% since 2023 compared to our favorite Green Line (Mortgage Rate) sitting well over 6% at the same time.

Phase 3: The “Stuck” Era (2024–2026)

Here’s the part that really stings. COVID-19 restrictions cooled off and supply chains got better over time causing average monthly inflation to drop from 8% to a more reasonable 2.4% by 2026. The Fed even threw us a bone by nudging Orange Line (Interest Rate) down to 3.75%.

But take a look at the chart the Green Line (Mortgage Rate) didn’t budge and barely go done since 2024. Neither did the Red Line (10-Year Treasury Yield). What’s going on here? A couple issues:

- The “We Predicted This” Factor: Investors in 2023 were already “anticipating” inflation and interest rates dropping when they bought 10-year Treasury Bonds. See how the Red Line (10-Year Treasury Yield) is less than the Orange Line (Interest Rate) in 2023, meaning investors didn’t ask for as much as they could have back then. So when Orange Line (Interest Rate) drops in 2024, the Red Line (10-Year Treasure Yield) barely changed.

- The 2% Goalpost: Ok. So easy to solve…The Fed can drop interest rates even lower, right? Right? Sorry, no dice…they don’t want to slash rates until inflation get below the magical 2% mark. Until then, we’re essentially stuck in economic purgatory.(https://www.usbank.com/investing/financial-perspectives/market-news/federal-reserve-tapering-asset-purchases.html).

- The Global Headache: Toss in some geopolitical spice—like the ongoing tensions with Iran and the stalemate in Ukraine—and you’ve got a market too nervous to lower its guard.

The Bottom Line

We are currently living in a high-market standoff where nobody has the leverage to blink first. If you’re waiting for those 3% mortgage rates to come back, you might want to get comfortable. We’re moving at the speed of the global economy now, and she’s not in a rushing mood.

In the future, we’ll dig into what might help move the needle other than waiting…stay tuned.

Data Sources for US Economic Metrics Chart:

Blue Line (Inflation Rate) https://fred.stlouisfed.org/graph/?g=1wmdD

Orange Line (Interest Rates) https://fred.stlouisfed.org/graph/?g=1Ng5J

Red Line (10-Year Treasury Bond Yield) https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve

Green Line (Mortgage Rates) https://www.freddiemac.com/pmms

Leave a comment